|

November 2022 Market Update

Chief Investment Officer Andy Stout provides an update on the market, the Fed, and latest information we are monitoring on your behalf.

#1 Stocks and bonds rally on hopes of a less aggressive Federal Reserve

The S&P 500 closed above the psychologically-important 4,000 level for the first time in two months. But it hasn’t been just large-cap stocks that performed well this quarter. Small-caps and international stocks have also posted solid gains. Even bonds are up this quarter, with long-term interest rates declining (interest rates and bond prices move in opposite directions).

The primary reason for the market strength has likely been the increasing probability that the Fed will slow down its rate hikes. The market is starting to expect this because of recent economic data pointing to sluggish economic growth and the growing influence of dovish Vice Chair Lael Brainard (doves tend to favor relatively lower interest rates).

While a slowing economy isn’t necessarily a good thing, a Fed that has to hike aggressively to fight inflation will slow down the economy significantly more down the road. So, in other words, it’s better to have a little less economic upside now to reduce the chance of a more considerable downside later.

#2 Last week’s mixed data emboldened the hopes of a 2023 Fed pivot

Helping to enhance the argument for a less aggressive Fed were some weak economic releases. For example, a preliminary look at the manufacturing and services sectors indicated a contraction in November. Additionally, initial jobless claims jumped from 223k to 240k, and continuing claims hit their highest level since early March. On a positive economic note, durable goods orders and new home sales beat economists’ forecasts. However, new home sales are well off their highs and are in a clear downtrend.

Also released last week were the November Fed meeting minutes, which showed a dovish tilt. The minutes expressed this view by stating most Fed members believe that inflation has peaked and that inflation expectations are anchored.

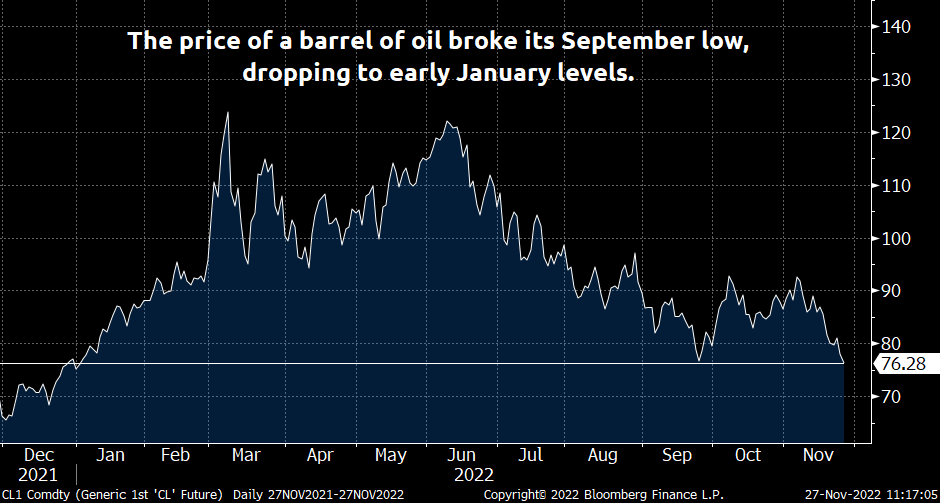

Adding to the moderating economic growth picture was oil closing at $76.28 a barrel, its lowest level since January. Contributing to these lower prices is the hypothesis that there is an oversupply of crude based on the belief that Russian oil will continue to flow to Europe and China’s ongoing lockdowns would further reduce demand.

#3 Data we are monitoring

With stock and bond markets taking their cues from the Fed, Wall Street will pay close attention to the 10 Fed speeches this week, including Fed Chair Jerome Powell’s discussion on Wednesday. The Fed is, of course, closely watching the job market and inflation data, and we’ll get critical updates on both this week. Specifically, economists expect the November jobs report to show that the unemployment rate remained at 3.7% and that employers added 200k new jobs. Further, economists believe the Fed’s preferred inflation measure, PCE, increased by 0.4% in October, causing the year-over-year inflation print to decelerate from 6.2% to 6%.

This week’s other notable economic releases are job openings, personal income, personal spending, jobless claims, and the ISM manufacturing survey.

Additionally, growing protests in China against Beijing’s Covid Zero policy could impact the market. Some companies have begun to feel the effects. For example, Bloomberg reported that Apple could face a shortfall of 6 million iPhone Pros this year because of unrest at the Chinese factory of one of its major suppliers.

Our team will analyze the newest information provided in these releases and evaluate our next steps accordingly. As always, please let us know if you have any questions about how this relates to your overall financial plan and goals.

November 28, 2022

All data, unless otherwise noted, is from Bloomberg. Past performance does not guarantee future results. Any stock market transaction can result in either profit or loss. Additionally, the commentary should also be viewed in the context of the broad market and general economic conditions prevailing during the periods covered by the provided information. Market and economic conditions could change in the future, producing materially different returns. Investment strategies may be subject to various types of risk of loss, including, but not limited to, market risk, credit risk, interest rate risk, inflation risk, currency risk, and political risk.

This commentary has been prepared solely for informational purposes and is not an offer to buy or sell, or a solicitation of an offer to buy or sell any security or instrument, or to participate in any particular trading strategy or an offer of investment advisory services. Investment advisory and management services are offered only pursuant to a written Investment Advisory Agreement, which investors are urged to read and consider carefully in determining whether such agreement is suitable for their individual needs and circumstances.

RAA, its affiliates, and its employees may have positions in and may affect transactions in securities and instruments mentioned in these profiles and reports. Some of the investments discussed or recommended may be unsuitable for certain investors depending on their specific investment objectives and financial position.

RAA is an SEC-registered investment advisor that provides advisory services for discretionary, individually managed accounts. To request a copy of RAA’s current Form ADV Part 2, please call our Compliance department at 916-482-2196 or via email at compliance@allworthfinancial.com.