|

May 2023 Market Update

Chief Investment Officer Andy Stout helps explain what triggered a handful of regional banks to fail, and what fallout could still lie ahead.

We all know market volatility is an inherent part of investing; it’s the risk we accept that allows us to help meet our financial goals. However, bank failures feel like a different type of risk because they can call into question the safety of our deposits.

Not surprisingly, we’ve received many inquiries about the regional banking crisis, so I wanted to take this opportunity to address these concerns.

2023’s Regional Banking Crisis

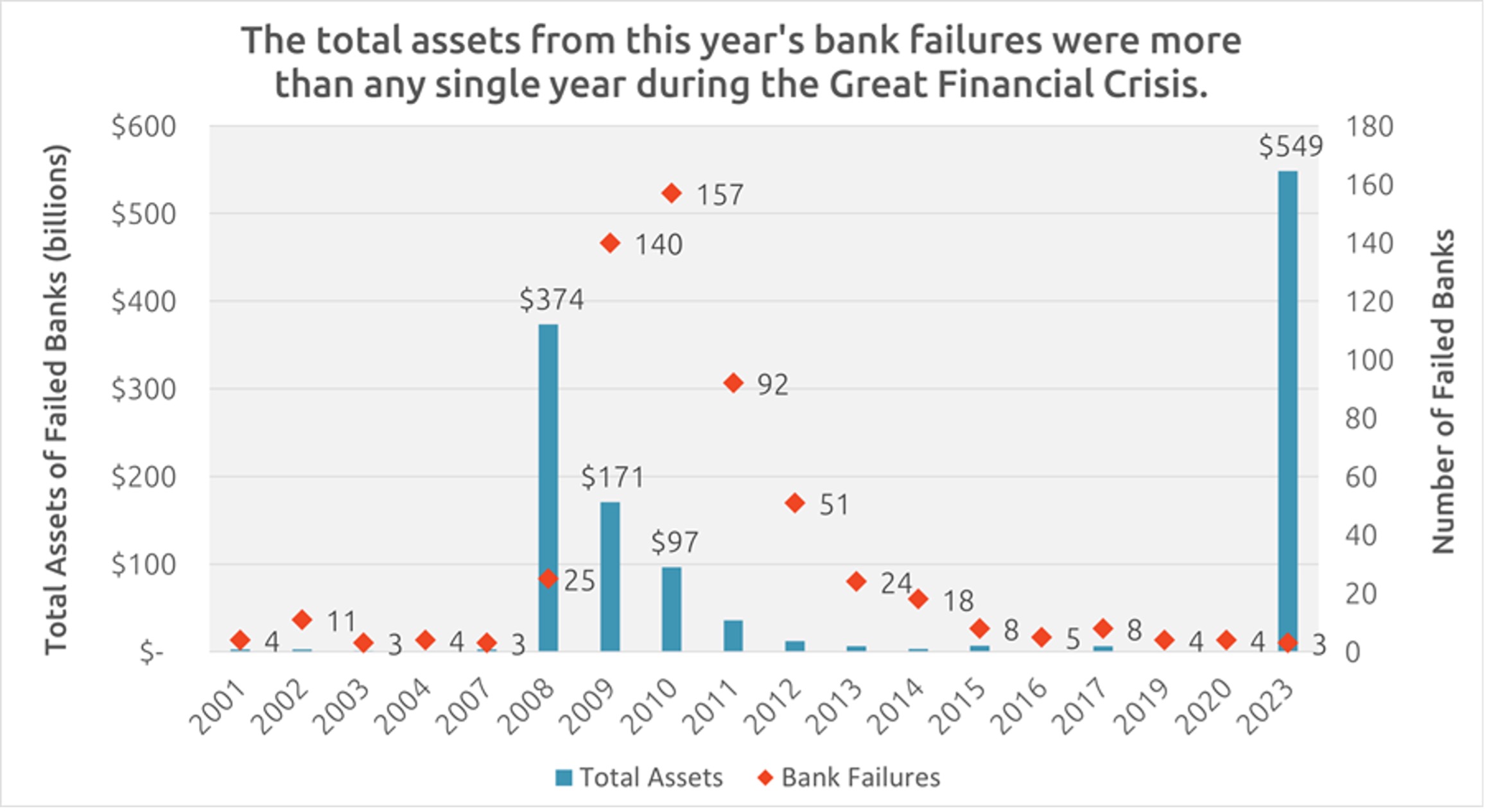

The numbers are staggering. Even though many more banks failed during the Great Financial Crisis, the assets from the three banks that collapsed this year easily exceeded any year during that downturn. Looking at the graph by itself suggests an environment rivaling 2008.

However, as you might expect, the true backdrop is much more nuanced. While the failures of Silicon Valley Bank, Signature Bank, and First Republic have unique characteristics, there are commonalities. For example, these banks had a significant percentage of deposits above the FDIC’s $250,000 limit, leaving them vulnerable to a bank run.

Additionally, these three banks suffered from taking excessive risks: Silicon Valley Bank focused on the tech start-up industry, Signature Bank had a cryptocurrency payment platform that may have dissuaded other banks from buying it before it failed, and First Republic was overexposed to jumbo loans made at very low interest rates.

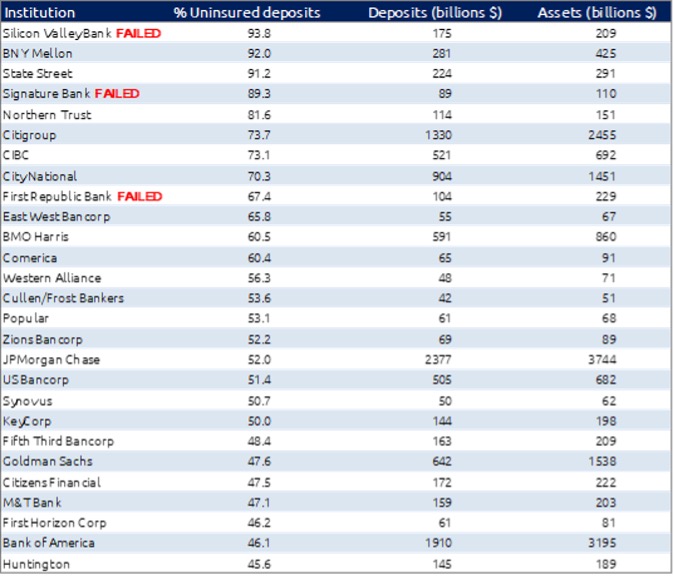

*Uninsured deposit percentage as of 12/31/22; Deposit and asset values as of 3/31/23 except for the failed banks, which are as of the failed date

A few notable names top the list, such as BNY Mellon and State Street. Analysts aren’t too worried about those banks because they focus mostly on businesses, not consumers. Drilling down into these banks’ balance sheets reveals that the percentage of business loans is 93% for BNY Mellon and 100% for State Street.

So far, we’ve discussed issues with three specific banks, but now I want to shift to the overarching problem.

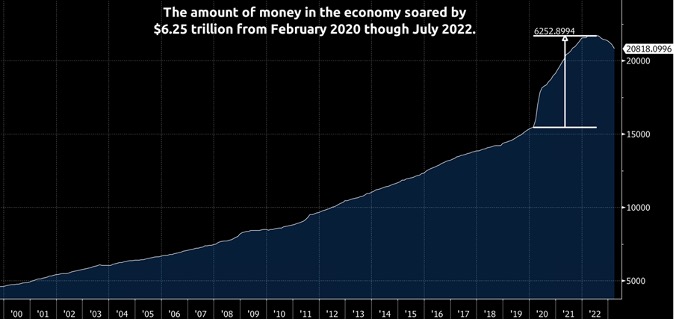

When Covid hit in 2020, the Federal Reserve (Fed) cut short-term interest rates to 0% and left them there for two years. In addition, the Fed implemented many programs to inject money into the economy to encourage economic growth, including the restart of quantitative easing (QE). We estimate the amount of monetary stimulus by computing the change in the Fed’s balance sheet, which more than doubled, soaring from $4.2 trillion to almost $9 trillion.

At the same time, Congress ramped up its spending through various fiscal policy actions, such as the CARES Act, which put another $2.2 trillion into the economy.

Some of this money was spent, some was invested in the markets, and a lot was saved. As a result, the total amount of money in the economy rose from about $15 trillion to almost $21 trillion, with much of that deposited at banks.

It was a common practice during this time for banks to use deposits to make long-term loans and buy long-term Treasury and agency bonds. This was an acceptable thing to do… until inflation became a problem.

The high inflationary environment forced the Federal Reserve (Fed) to go on one of its most aggressive interest rate hiking campaigns ever. This has helped consumer inflation fall from 9.1% in June 2022 to 4.9%.

However, these rate hikes also pushed down the value of the loans issued and bonds purchased (interest rates and bond/loan values move in opposite directions). Subsequently, banks became worth less than what they were last year. Additionally, savers demanded higher interest rates on their deposits, but many banks couldn’t offer that because their assets were tied up in bonds and loans with large amounts of unrealized losses.

To help address this macro issue, the Fed offered to loan money to banks if they put those bonds they bought up as collateral. The key to that offer was that the value of the bonds would be their "par value," not the current lower value (par value is the bond’s price at maturity). In other words, the Fed backstopped banks for their mismanagement.

This bailout has worked so far as banks have borrowed more from the Fed while, at the same time, there’s been a decline in emergency lending. Additionally, the deposit outflow has stabilized. There could be other small and mid-sized regional banks to struggle, but larger banks don’t appear to be a concern.

But without a comprehensive solution, depositors at smaller banks may flee to the safety of larger banks. One idea being floated is unlimited FDIC insurance. While that would likely encourage small-bank depositors to keep their money at their bank (a good thing), it could lead to moral hazard, meaning banks could take on material risks because the added protections mean that there wouldn’t be any negative consequences (a very bad thing).

The Economic Fallout

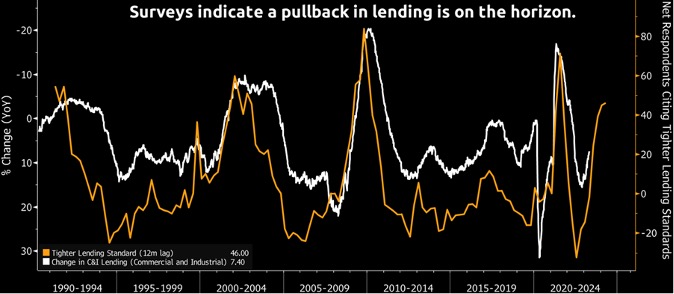

While a large-scale financial crisis is highly unlikely, that doesn’t mean there won’t be an impact. Banks are in the process of tightening their lending standards (i.e., higher rates on loans and loans made to more credit worthy borrowers).

The following graph shows that 46% of loan officers said they had tightened lending standards (orange line), which often leads to a decline in loan volume. Consequently, this could result in less spending and slower economic growth.

This economic uncertainty is why the market expects the Fed to cut interest rates later this year. However, there is still concern about inflation, specifically that inflation expectations are less anchored. We observe this in longer-term inflation expectations (the 5-10 year period) rising to 3.2%, its highest level in more than 10 years. This raises the risk that inflation is becoming more entrenched in the economy, leading to a chance the Fed could lift rates at its next meeting on June 14.

This article was intended to inform you about the regional banking crisis and its potential implications. It was also to let you know that it’s impossible to predict how this will unfold. Subsequently, we are modeling multiple economic scenarios, which enables us to position your investments to help protect your money.

May 19, 2023

All data unless otherwise noted is from Bloomberg. Past performance does not guarantee future results. Any stock market transaction can result in either profit or loss. Additionally, the commentary should also be viewed in the context of the broad market and general economic conditions prevailing during the periods covered by the provided information. Market and economic conditions could change in the future, producing materially different returns. Investment strategies may be subject to various types of risk of loss including, but not limited to, market risk, credit risk, interest rate risk, inflation risk, currency risk and political risk.

This commentary has been prepared solely for informational purposes, and is not an offer to buy or sell, or a solicitation of an offer to buy or sell, any security or instrument or to participate in any particular trading strategy or an offer of investment advisory services. Investment advisory and management services are offered only pursuant to a written Investment Advisory Agreement, which investors are urged to read and consider carefully in determining whether such agreement is suitable for their individual needs and circumstances.

RAA and its affiliates and its employees may have positions in and may affect transactions in securities and instruments mentioned in these profiles and reports. Some of the investments discussed or recommended may be unsuitable for certain investors depending on their specific investment objectives and financial position.

RAA is an SEC-registered investment advisor that provides advisory services for discretionary individually managed accounts. To request a copy of RAA’s current Form ADV Part 2, please call our Compliance department at 916-482-2196 or via email at compliance@allworthfinancial.com.